“A man should never neglect his family for business.” —Walt Disney

Quick Answers: Will Updating My W4 Tax Form Increase My Paycheck?

- Child Tax Credit (CTC) is going up to 2.2K per child, but many will need to update their W4 to see that reflected in their paycheck.

- The One Big Beautiful Bill Act (OBBBA) added new family benefits (like child savings accounts and enhanced dependent care credits). Your W4 is how you unlock those benefits in real-time.

- A “too big” refund means you’re overpaying the IRS. That’s money you could be using during the year (though if you prefer a forced savings plan, that’s your choice).

- Use the IRS Tax Withholding Estimator and review your W4 tax form to make sure you’re not overpaying on taxes.

I talked with a new Milwaukee client not long ago. Married. Two-year-old at home. And yet… his W-4 was still marked as single, zero dependents.

He was getting huge refund checks every spring. That may sound great, but the truth is he was overpaying the IRS thousands during the year. On top of that, he was missing out on key credits and deductions that would minimize his tax burden throughout the year.

That was money that could have been covering groceries, daycare, or even just easing the stress of bills.

I see too many people like this client, quietly letting the IRS hold onto their money all year long, interest-free.

Especially with the One Big Beautiful Bill Act (OBBBA) now in effect, getting your W4 right is the key to more take-home pay for your family.

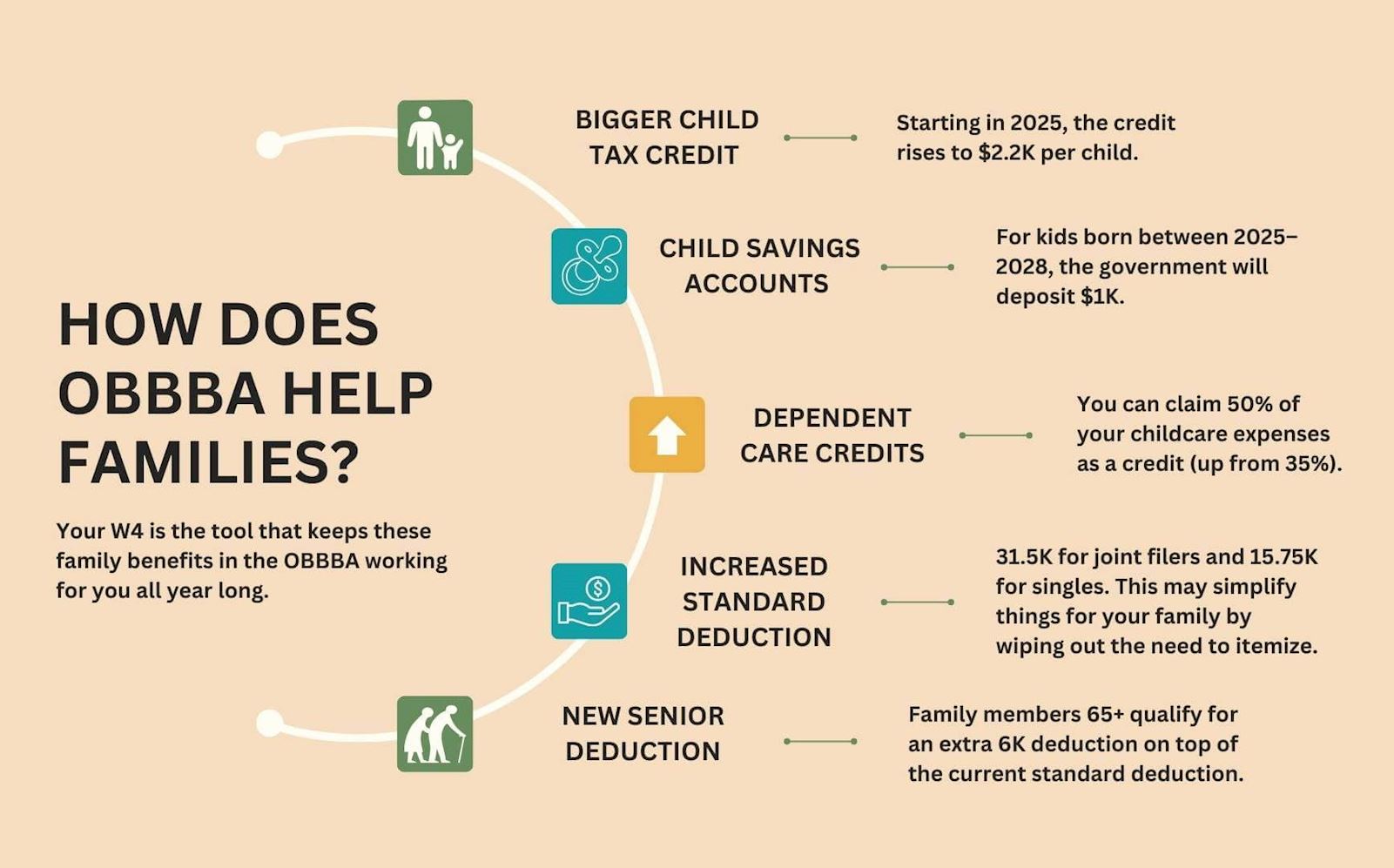

How Does the OBBBA Help Southeastern Wisconsin Families?

Your W4 is the tool that keeps these family benefits in the OBBBA working for you all year long:

Bigger Child Tax Credit (CTC):

Starting in 2025, the credit rises to 2.2K per child (subject to income phaseouts). If your W4 tax form doesn’t reflect your dependents, you’ll keep waiting for a big refund check instead of seeing that money show up throughout the year.

Child Savings Accounts:

For kids born between 2025–2028, the government will deposit 1K. While that isn’t tied directly to the W4, your overall tax planning (and how you report dependents) makes this fit into your bigger family picture.

Enhanced Dependent Care Credits:

With the OBBBA, you can now claim 50 percent of your childcare expenses as a credit, up from 35 percent. This means most families will get a 15-percentage-point increase in their credit. But only if your withholding strategy is built with this in mind.

Increased Standard Deduction (now permanent):

31.5K for joint filers and 15.75K for singles. This may simplify things for your family by wiping out the need to itemize, while also lowering your taxable income.

New Senior Deduction (2025–2028):

Got parents or grandparents in the home? Family members 65+ qualify for an extra 6K deduction on top of the current standard deduction (this phases out as income rises). So make sure your W4 is tailored to your current family structure.

How Do I Get More Money for My Family?

So what do you do right now? Three things:

- Update your W4 tax form (today). Don’t let outdated info linger. The IRS has a great online tool, the Tax Withholding Estimator, that can help you figure out the correct withholding. But, if you have a complex financial situation (like self-employment income, capital gains, or specific itemized deductions), it’s best to consult with a professional (wink wink) to make sure you’re getting it right.

- Get a review of your full situation. Beyond the W4, we’ll sit down together and check for every credit and deduction you qualify for. Married filing jointly? Dependents in daycare? Elderly parent at home? Let’s make sure every piece of your life is reflected in your tax picture.

- Plan for 2025 and beyond. Tax legislation (like OBBBA) changes the landscape. We’ll talk about college savings (529 plans), estate planning moves, and how to position your family for maximum tax benefits.

FAQs

“How often should I update my W4?”

At least once a year, and always after major life changes (marriage, divorce, new baby, job change, starting a side gig or self-employment, etc.).

“If I change my W4 now, will I owe more at tax time?”

Not necessarily. The aim with adjusting your W4 is to get your withholding as close to your actual tax liability as possible. So, if you set it correctly, you won’t have a big refund or a big tax bill.

This gives you more money in each paycheck throughout the year, so you have control of your cash flow instead of giving the government an interest-free loan. And it helps you avoid underpayment penalties.

“What happens if I don’t update my W4 after OBBBA?”

You’ll likely miss out on seeing the increased credits and deductions reflected in your take-home pay. That means waiting until refund season to get your money back.

“Can my employer help me fill out my W4?”

Your employer can provide the form, but they can’t give you personalized tax advice. Legally and ethically, they’re not qualified to tell you how to fill it out. A tax professional can help you accurately calculate the correct withholding based on your specific financial situation. So, when you meet with your tax pro, be sure to bring your most recent pay stub and tax return.

“I like getting a big refund. Should I still adjust my W4?”

That’s your choice, but remember: a large refund is just your own money being returned to you. It’s essentially an interest-free loan you gave to the government throughout the year. With that cash flow, you could pay down debt, invest it, or put it into a high-yield savings account where it can earn interest for you.

“How do I adjust my W4 if I work multiple jobs or my spouse also works?”

Likely, you’ll need to use the “Two-Jobs/Multiple Jobs” section on your W4 for the highest-paying job and leave the other W4s blank or use a higher withholding amount.

The IRS Withholding Estimator tool is helpful here because it lets you input income from all sources to get a more accurate picture. However, we can also look at your combined income and help you fill out the W4 forms for each job.

When you manage your taxes right, you get to make sure your paycheck works harder for your family every single pay period.

And when we adjust your W4 correctly, you don’t have to wait until next spring to see the benefits. You’ll feel it in your regular take-home pay. With more breathing room for childcare, groceries, or savings.

My team and I want to help you apply the new OBBBA changes in a way that maximizes what your family keeps throughout the year. So, let’s sit down and look at your W4 together:

414-325-2040